50대 이후, 늦지 않은 노후 준비의 기술: 경제 콘서트에서 배운 핵심 전략

"늦었다고 생각할 때가 가장 빠르다." 이 말처럼, 노후 준비는 언제 시작하든 의미가 있습니다. 최근 열린 27번째 경제 콘서트에서는 은퇴 전문가 김경록 박사가 노후 준비의 중요성과 실질적인 방법을 제시하며, 참석자들에게 깊은 인사이트를 제공했습니다. 이 글에서는 강연의 주요 내용을 바탕으로, 50대 이상의 독자들이 실천할 수 있는 노후 준비 전략을 정리해 보았습니다.

21세기 세대, 노후를 고민하다

우리는 역사상 처음으로 은퇴 후 삶이 은퇴 전보다 길어질 가능성이 높은 세대입니다. 과거에는 은퇴 후 몇 년만 살았던 반면, 이제는 20년 이상을 계획해야 하는 상황이죠. 하지만 학교나 직장에서 은퇴 이후의 삶을 가르쳐 주지 않기 때문에, 각자가 스스로 준비해야 합니다.

노후 준비의 핵심 요소: 주거, 건강, 금전

노후 준비는 단순히 돈을 모으는 것을 넘어섭니다. 안정적인 주거 환경, 건강 관리, 그리고 효율적인 재정 계획이 필수적입니다. 강연에서는 특히 국민연금과 자산 관리를 통한 안정된 노후 생활의 중요성이 강조되었습니다.

1. 국민연금과 사적 연금 활용

- 국민연금은 기본적인 소득을 보장하는 주춧돌입니다. 월 100만 원의 국민연금을 받는다면 그 가치는 약 3억 원에 달합니다.

- 퇴직연금(IRP) 등 사적 연금을 적극적으로 활용하여 추가 소득원을 마련하세요.

2. 주택 자산 활용

- 주택 연금은 고정 소득이 부족한 경우 유용한 선택지가 될 수 있습니다.

- 거주 중인 집을 자산 증식 수단으로 활용해보세요.

3. 금융 자산 관리

- 물가 상승률 이상으로 자산을 운용해야 합니다. 안정성과 수익성을 겸비한 포트폴리오를 구성하세요.

- 리스크를 분산시키기 위해 다양한 투자 상품에 분배하는 것이 중요합니다.

노후 빈곤: 일본 사례에서 배우다

일본의 사례는 우리에게 중요한 교훈을 줍니다. 일본에서는 연금 사각지대에 있는 사람들이 노후 빈곤에 빠지는 경우가 많습니다. 예를 들어:

- 중대한 질병으로 인해 치료비가 소진되는 경우

- 임대료 부담으로 인해 주거 불안정성을 겪는 경우

- 가족 돌봄으로 경제활동이 중단된 경우

한국에서도 비슷한 위험이 존재하지만, 국민연금과 평균 자산 수준(약 5억 원)이 이를 완화하는 데 도움을 줍니다.

미래를 위한 실질적인 전략

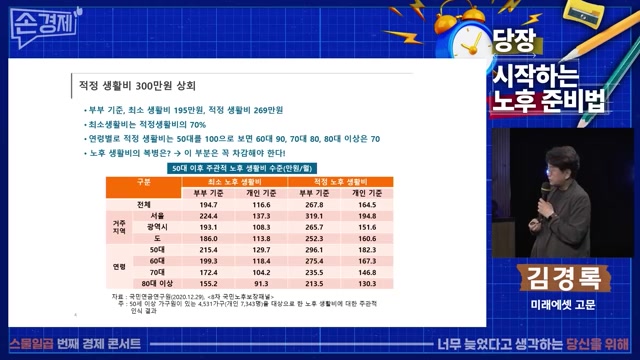

1. 적정 생활비 계산하기

서울 기준으로 현재 적정 생활비는 약 340만 원이며, 이는 향후 20년 뒤 약 700만 원까지 증가할 수 있습니다. 이를 대비하려면:

- 매년 물가 상승률(약 4%)을 고려한 자산 관리가 필요합니다.

- 현금을 보유하기보다는 물가 상승률 이상 수익을 내는 자산에 투자하세요.

2. 소득 감소 대비

50대 이후 소득은 평균적으로 약 40% 감소합니다. 이를 보완하기 위해:

- 재취업이나 파트타임 근무를 고려하세요.

- 지출 구조를 점검하고 필수 지출 항목을 유지 가능한 수준으로 조정하세요.

3. 상속 및 인적 자산 활용

- 상속 자산도 노후 계획에 포함하여 효율적으로 관리하세요.

- 자신의 전문성을 키워 재취업 시장에서 경쟁력을 확보하세요.

아직 늦지 않았다

탈무드에는 "이미 끝난 일을 후회하기보다는 하지 못한 일을 후회하라"는 말이 있습니다. 노후 준비도 마찬가지입니다. 지금 시작하면 늦지 않았습니다. 작은 습관부터 바꾸고, 꾸준히 실행해 나간다면 안정된 미래를 맞이할 수 있을 것입니다.

여러분은 어떤 노후를 꿈꾸고 계신가요? 지금부터라도 한 걸음씩 준비해보세요!

#노후준비 #경제콘서트 #국민연금 #퇴직연금 #주택연금 #재테크 #50대재무관리 #노후빈곤예방 #자산관리 #재취업

[손경제][콘서트] 50대, 이미 늦었다고 생각하는 당신을 위한 노후준비법 (김경록 미래에셋자산운

50대 이상을 위한 **노후 준비법**을 다룬 이번 강연은 미래를 대비하는 모든 이에게 귀중한 정보를 제공합니다. 전문가는 **경제적 어려움**을 피하기 위해 필요한 요소로 주거, 건강, 금전 준비

lilys.ai

Preparing for Retirement After 50: Key Strategies from the Economic Concert

"It's never too late to start." This timeless saying perfectly applies to retirement planning. At the 27th Economic Concert, retirement expert Dr. Kyung-Rok Kim shared invaluable insights on preparing for a secure and fulfilling retirement. This article distills the key takeaways from his talk, offering practical strategies for readers over 50 to begin or refine their retirement plans.

A Unique Challenge for the 21st Century Generation

For the first time in history, we are a generation that may spend as much time in retirement as we do working. While previous generations only needed to plan for a few years post-retirement, today’s retirees must prepare for decades. Yet, schools and workplaces rarely teach us how to navigate this phase of life, leaving individuals to figure it out on their own.

The Three Pillars of Retirement: Housing, Health, and Finances

Retirement preparation goes beyond saving money. It requires a holistic approach that includes stable housing, health management, and financial planning. Dr. Kim emphasized leveraging public pensions and asset management to ensure financial security in later years.

1. Maximize Public and Private Pensions

- Public pensions like Korea’s National Pension System provide a foundational income. For example, receiving 1 million KRW monthly from this system is equivalent to having 300 million KRW in assets.

- Supplement this with private pensions like Individual Retirement Plans (IRPs) to create additional income streams.

2. Utilize Housing Assets

- Reverse mortgages can be an excellent option for those with limited cash flow.

- Consider how your home can serve as both a living space and a financial resource.

3. Manage Financial Assets Wisely

- Aim for investment returns that outpace inflation by diversifying your portfolio.

- Spread risk across various investment products to safeguard your wealth.

Lessons from Japan: Avoiding Retirement Poverty

Japan offers critical lessons on the risks of inadequate retirement preparation:

- Major illnesses can drain savings.

- High rental costs can lead to housing instability.

- Caregiving responsibilities may force individuals out of the workforce.

In Korea, similar risks exist but are mitigated by the National Pension System and an average household net worth of approximately 500 million KRW.

Practical Strategies for a Secure Future

1. Calculate Your Living Expenses

In Seoul, the current average monthly living cost is around 3.4 million KRW, which could rise to 7 million KRW in 20 years due to inflation. To prepare:

- Account for annual inflation (approximately 4%) in your financial planning.

- Invest in assets that yield returns above inflation rates rather than holding cash.

2. Prepare for Reduced Income

Income typically decreases by about 40% after age 50. To address this:

- Explore part-time work or reemployment opportunities.

- Audit your spending and adjust essential expenses to sustainable levels.

3. Leverage Inherited and Personal Assets

- Include inheritance in your financial planning and manage it strategically.

- Enhance your skills to remain competitive in the job market.

A Positive Outlook: It's Never Too Late

The Talmud says, "Regret not what is already done but what you have yet to do." The same applies to retirement planning—starting now is better than not starting at all. By making small changes and staying consistent, you can build a stable future.

What kind of retirement do you envision? Take the first step today toward making it a reality!

#RetirementPlanning #EconomicConcert #NationalPension #PrivatePension #ReverseMortgage #FinancialPlanning #Over50Finance #AvoidRetirementPoverty #AssetManagement #Reemployment

'이슈 > 경제' 카테고리의 다른 글

| 트럼프 시대의 경제 정책과 한국: 무역 흑자의 비밀을 파헤치다 (0) | 2025.03.11 |

|---|---|

| 전기 요금 지역 차등제, 정말 공정한 해결책일까? (1) | 2025.03.10 |

| 중국인 건강보험 논란, 진짜 문제는 무엇일까? (1) | 2025.03.10 |

| 실패를 두려워하는 사회, 한국의 혁신을 가로막다 (0) | 2025.03.10 |

| "인플레이션, 우리 삶에 숨겨진 세금 이야기" (6) | 2025.03.08 |